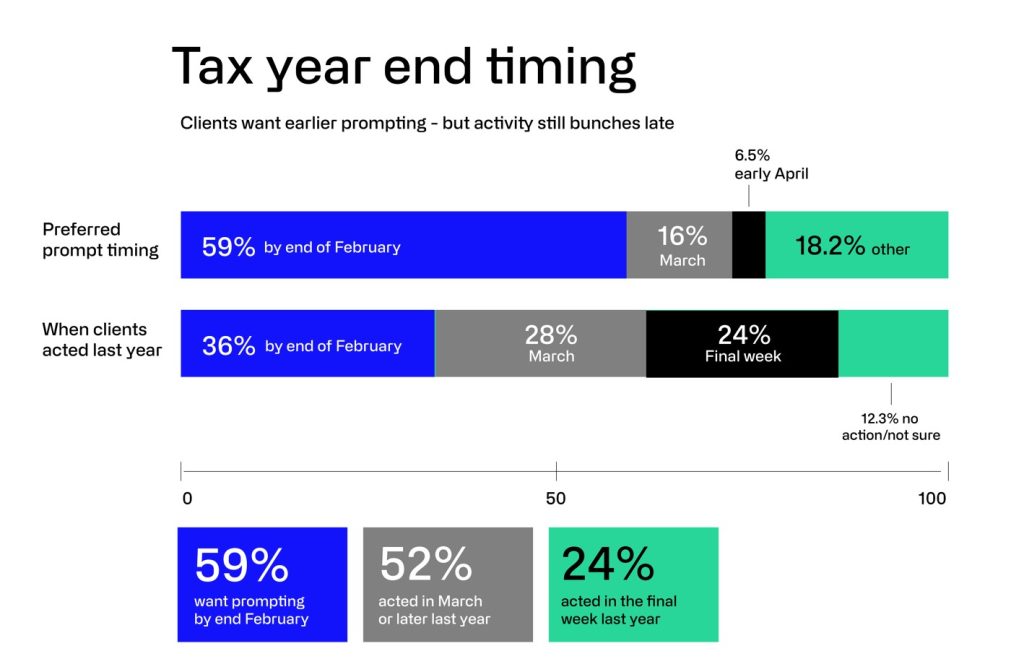

Nearly a quarter acted in the final week last tax year. That’s not “bad behaviour” – it’s an engagement and process problem.

A useful rule of thumb – if something happens every year, it’s not a surprise – it’s a system. And the late rush is a system.

In our research*, 24% of advice-engaged clients did most of their tax-year-end activity in the final week last year (including a meaningful subset in the last 2–3 days). That’s not a “people are flaky” story. It’s a “we left the decision too late” story.

Here’s the kicker – when we ask clients when they prefer to be prompted, the market votes for earlier than most firms currently behave. 59% want to hear by end of February, while just 6.5% prefer contact in early April. In other words: clients don’t want the adrenaline. They want the runway.

So, the practical opportunity is obvious – turn tax year end into a two-stage process.

- End Feb / early March confidence-building check: A short, structured review: “Here are the 2–3 things worth doing before 5 April; here’s what we can defer.”

- Late March execution window: Admin-ready, documentation-ready, decisions already framed.

Why does this matter commercially? Because the late rush is expensive. It increases suitability risk, creates operational bottlenecks, forces hurried conversations, and drives avoidable client anxiety. It also dilutes your best advice – not because it’s wrong, but because it arrives when clients are least ready to act.

Tax year end is one of the few moments where you can make “proactivity” visible and a firm that has a repeatable system signals competence.

Treat this as a design challenge – create a calendar prompt, a one-pager, a simple upload checklist, and a clear “decision menu” (do now / do soon / park). You’re not just improving outcomes. You’re reducing friction – and friction is what turns good intentions into no action.

*Based on research commissioned by Wealthtime and conducted by Ad Lucem.

The survey, conducted in January 2026 among 1,000 UK adults aged 35+ with average investable assets of £350,000, provides critical insights into the behaviours, concerns and preferences of people navigating tax year-end planning.

Please be aware that Wealthtime is not responsible for the information displayed on, or the availability of, the Ad Lucem website.

Download the reportRead the next article

For more tax year end planning top tips, read the next bitesize article.

Read nextBrowse all bitesize articles

For more expert insight and analysis, visit our tax year end library.

Visit the libraryStay connected

This article is intended for regulated financial advisers and investment professionals only.