Tony Wickenden, Technical Connection

As the end of the tax year approaches, serious consideration should be given to any unused allowance or exemption that is only available on a “use it or lose it” basis — because it cannot be carried forward to the next tax year. One of these is the annual Capital Gains Tax (CGT) exemption of £3,000.

So, let’s examine the realities that need to be considered in relation to its use:

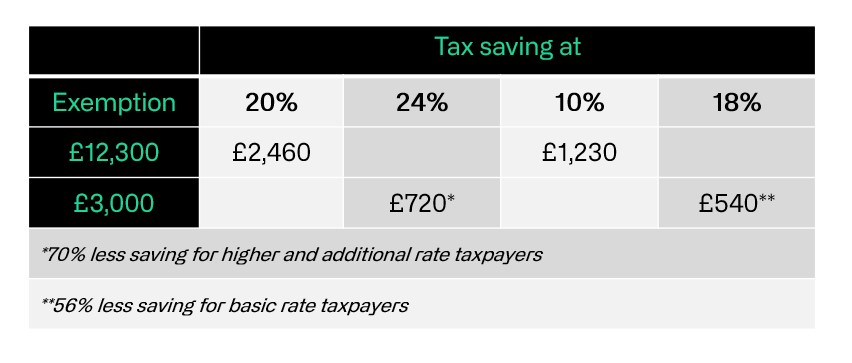

- Since the change to the CGT rates that happened on 30 October 2024 (24% for additional and higher rate taxpayers and 18% for basic rate taxpayers) the tax benefit from using the exemption will be £720 and £540 respectively.

- Where a disposal was going to take place anyway (for economic/commercial reasons) any relief/exemption is to be welcomed.

- If action is taken purely on tax grounds, then a cost/benefit assessment needs to be undertaken:

The benefit is the tax saving illustrated above in point 1 – but it will not be a current benefit. At the earliest it will, in most cases, be secured when the tax would otherwise be due on the disposal in January 2027. But where the investor wishes to bank the use of the exemption but remain invested, a disposal followed by reacquisition will be necessary. In that case the benefit will be realised in the shape of a lower chargeable gain when an eventual permanent disposal of the asset is made. At that point the gain will be measured taking account of the acquisition price when the reinvestment was made, which will be higher to the extent of the annual exemption used earlier. It’s also important to keep in mind that to achieve the desired outcome it will not be possible to reacquire the same assets as those disposed of within 30 days of the disposal. As a result, it will be necessary to stay out of the market for that length of time, or reacquire something similar but not identical, or have someone else who is closely associated with you (e.g. a spouse), make the reacquisition.

The cost will be seen in the costs associated with the disposal and, where relevant, reacquisition. Both current costs are incurred to secure a future benefit. There will also be the time and effort cost of the action(s).

Used regularly to raise the eventual acquisition price, this strategy can deliver worthwhile eventual CGT saving. However, the drop in the annual CGT exemption from £12,300 (in tax year 2022/23) to its current level of £3,000 cannot be ignored – though it is ameliorated somewhat by the additional value of the saving at those higher rates.

Consider this comparison:

The drop in the annual CGT exemption from £12,300 (in tax year 2022/23) to its current level of £3,000 cannot be ignored – though it is ameliorated somewhat by the additional value of the saving at those higher rates.

Tony Wickenden, Technical Connection

Read the next article

For more tax year end planning top tips, read the next bitesize article.

Read nextBrowse all bitesize articles

For more expert insight and analysis, visit our tax year end library.

Visit the libraryStay connected

This article is intended for regulated financial advisers and investment professionals only.

The statements and opinions expressed in this article are those of the author and don’t necessarily reflect those of Wealthtime or any of its employees. The company does not take any responsibility for the views of the author.

The above is based on understanding of current law and HMRC practice, and Government proposals regarding future law and HMRC practice, as at 23 February 2026, and are presented for general consideration only and no action must be taken or refrained from based on the content of this article alone. Each case depends on its own facts and advice is essential. Accordingly, neither Wealthtime nor Technical Connection, nor any of their officers or employees can accept any responsibility for any loss occasioned as a result of any such action or inaction.